Insurance in a hard market – what it means for your business

All types of business experience cycles of expansion and contraction, and this is particularly true of the insurance industry. A number of factors influence these cycles – and in turn, these have an impact on insurance premiums.

Here we explain what’s happening in the insurance market, the effects it can have, and, more importantly, what you can do to minimise the impact on your business.

What is a hard market vs. a soft market?

Insurance industry cycles typically last from two to ten years and incorporate phases marked by an expansion and a contraction of insurance availability. After experiencing a soft market in the insurance industry for many years we are now facing a hard market.

- The characteristics of a soft market in the insurance industry include:

- Lower insurance premiums

- Broader coverage availability

- Relaxed underwriting criteria, which means underwriting is easier

- Increased capacity, which means insurance carriers write more policies and higher limits

- Increased competition among insurance carriers

- Ultimately these rate reductions associated with a soft market affect the insurance carriers’ bottom line, as an insurer relies on a combination of insurance premiums and investment income to make a profit as a company.

- On the other hand, the characteristics of a hard market include:

- Higher insurance premiums

- More stringent underwriting criteria, which means underwriting is more difficult

- Reduced capacity, which means insurance carriers write less insurance policies

- Less competition among insurance carriers.

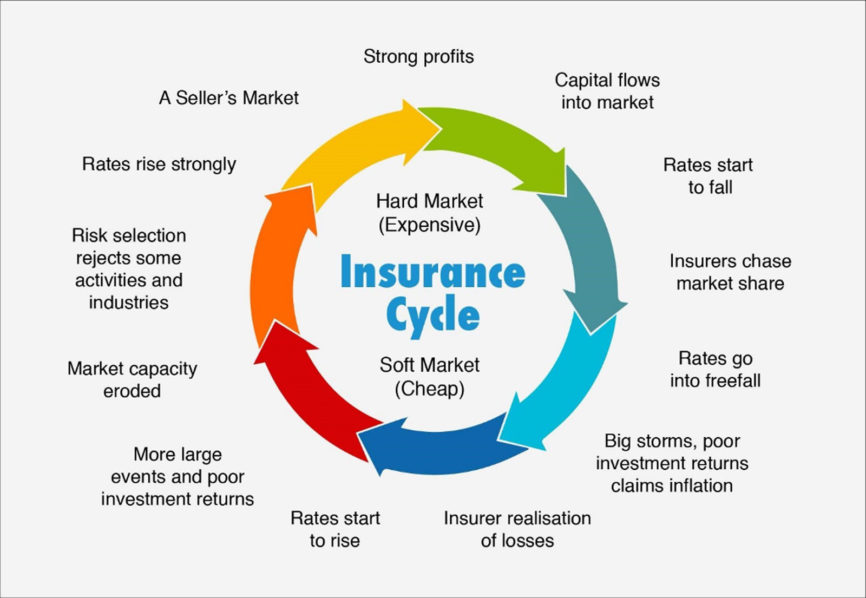

This diagram shows typical insurance cycle. We are currently transitioning from the dark blue to red zones:

Why are we currently facing a hard market?

Several factors have caused this rapid hard market:

- Launched in 2016, Solvency II which applies across the whole of the EU, placed a requirement on UK insurers to more than double their spare capital requirements to ensure they remain solvent and can meet the cost of claims pay-outs. This has led to a number of insurers leaving the market whilst others have significantly reduced their underwriting appetite and capacity to manage this.

- The Ogden discount rate is a calculation used to determine how much money insurance companies should pay as compensation to people who have suffered life-changing injuries so that it will cover all their predicted future losses. When the Minister of Justice changed the Ogden table rate in December 2016, it meant that insurers had to pay out far more on larger personal injury claims. This figure shocked the insurance world, as reserves on catastrophic injury cases had the potential to double – or worse.

- The insurance industry has endured persistent high loss ratios since 2013, primarily caused by an increase in frequency of severe property losses. Property rates in the UK were already far too low as we entered 2020 (affecting most commercial insurance policies). Soft market rating had become completely uneconomic. Even if we ignore the terrible recent events, insurers needed property rates to increase considerably in 2020.

- With property accounts already losing money, the last thing UK insurers needed were floods caused by storms Dennis and Ciara, estimated to cost well over £400 million. Climate change is causing insurers to struggle with correctly predicting floods, and they need to build up a pot of money to take care of the next set of bad floods which will inevitably be on their way as we head into winter.

- Reinsurance is a key component of an insurer’s pricing model and rates will rise significantly leaving insurers with no option other than to reflect these increases in their premium rates and to reduce their market capacity.

- When interest rates are high, insurers can get away with a certain amount of underwriting losses as they generate substantial investment income. Unfortunately, this is no longer the case, as the current interest rates are the lowest in the Bank of England near 300-year history. Insurers therefore have no option but to increase rates to balance their books.

- Finally, it is estimated that the combination of Covid-19 insurance claims, reduction in business and investment losses will cost the worldwide industry in excess of £200 billion, making it the most expensive insurance event ever. Clearly the current FCA test cases will have a significant bearing on how much the UK insurance industry will have to pay out in Business Interruption losses relating to Covid-19 but this is unlikely to be determined for several months.

This leaves us in the midst of rising insurance rates at a time when business risks are seemingly more prevalent than ever. Cyber breaches, climate change, pandemic, trade and professional risks are at the top of mind for most business owners.

Insurers are in the business of taking risks but given the rapid hardening of premium and terms, businesses with a strong risk management perspective and a track record of low claim activity can avoid the sweeping increases of premiums and terms, likely to affect the majority of UK businesses.

What you can do to ensure the effects of the hard market are kept to a minimum for your business

- Work with a specialist insurance adviser – the team at FOCUS has been advising clients for over 30 years and we have strong relationships with insurers and their underwriters.

- Invest in Risk Management – such as Health and Safety, Property Protection, Cyber Training for your staff etc.

- Make sure your insurance cover is updated to reflect any changes in your business – keeping in touch with your insurance provider is crucial to make sure you have the right cover in place – and not paying for cover you don’t need – or being underinsured.

- Avoid making claims for small losses – leave your insurance to pay out for significant events.

- When it comes to the renewal of your insurance, consider starting the process early and respond quickly to requests for information and documents.

Now is the time to step back and reassess how risk is managed within your business. Talk to FOCUS about your insurance arrangements and risk management solutions.

We’re here to help.

More in Insurance

Managing risk in a turbulent market – why trade credit insurance...

Cash flow is the lifeblood of any business, yet in today’s volatile economy, maintaining it is challenging. A robust risk management strategy that includes trade credit insurance can provide a vital safety net when customers or suppliers fail to pay.

Last Chance: Claim Your COVID-19 Business Interruption Compensation Before It’s Too...

As the March 2026 deadline approaches, businesses that suffered losses during the COVID-19 pandemic have a final opportunity to claim compensation under Business Interruption (BI) insurance policies. Recent legal changes mean more companies may now qualify, even if they were previously denied. If your business had BI cover in place during the first lockdown, now is the time to review your policy, seek expert advice, and act before your chance to recover pandemic-related losses is gone for good. Don’t miss out – find out what steps you need to take before it’s too late.

Act now to protect your business – up to 50% off...

The recent cyber-attacks on M&S, Co-op and Harrods show us that if big brands with full-time security teams can be compromised, no one is immune and all businesses are at risk.

From this author

Managing risk in a turbulent market – why trade credit insurance...

Cash flow is the lifeblood of any business, yet in today’s volatile economy, maintaining it is challenging. A robust risk management strategy that includes trade credit insurance can provide a vital safety net when customers or suppliers fail to pay.

Last Chance: Claim Your COVID-19 Business Interruption Compensation Before It’s Too...

As the March 2026 deadline approaches, businesses that suffered losses during the COVID-19 pandemic have a final opportunity to claim compensation under Business Interruption (BI) insurance policies. Recent legal changes mean more companies may now qualify, even if they were previously denied. If your business had BI cover in place during the first lockdown, now is the time to review your policy, seek expert advice, and act before your chance to recover pandemic-related losses is gone for good. Don’t miss out – find out what steps you need to take before it’s too late.

Act now to protect your business – up to 50% off...

The recent cyber-attacks on M&S, Co-op and Harrods show us that if big brands with full-time security teams can be compromised, no one is immune and all businesses are at risk.